Point of Care Diagnostic Market Size, Forecast 2025-2032

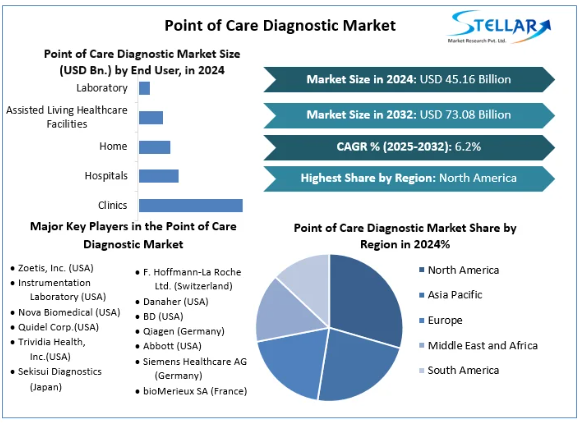

Point of Care Diagnostic Market size was valued at USD 45.16 billion in 2024 and is expected to reach USD 73.08 billion by 2032, at a CAGR of 6.2%.

Market Estimation & Definition

Point-of-care diagnostics refer to medical testing performed at or near the site of patient care. These tools offer rapid diagnostic results and enable clinicians to make timely decisions without relying on centralized laboratory infrastructure. POC tests are used in settings such as hospitals, clinics, emergency rooms, community health centers, and even at home.

By 2024, the market had reached USD 45.16 billion in value, largely driven by innovations in glucose monitoring, infectious disease testing, and mobile diagnostic platforms. By 2032, market projections point toward a robust USD 73.08 billion, highlighting how integral these diagnostics are becoming to modern healthcare systems.

Market Growth Drivers & Opportunities

Rising Burden of Infectious and Chronic Diseases

Globally, the healthcare industry continues to combat the spread of infectious diseases such as tuberculosis, HIV/AIDS, and COVID-19. The burden of these illnesses remains high, with millions of new cases reported annually. Early diagnosis is critical, and point-of-care tests provide a faster alternative to traditional laboratory tests, especially in under-resourced settings.

Chronic diseases, particularly diabetes and cardiovascular conditions, are also on the rise. The demand for real-time monitoring of blood glucose and heart-related biomarkers is encouraging the use of portable and wearable diagnostics.

Shift Toward Decentralized and Home-Based Care

The COVID-19 pandemic accelerated the adoption of remote care and decentralized healthcare delivery. This shift has continued post-pandemic, with patients and providers increasingly relying on at-home testing and mobile health tools. Point-of-care diagnostics serve this need by enabling users to access quick results without hospital visits, reducing both healthcare system burden and cost.

Healthcare systems are increasingly realizing cost benefits from such models. For example, treating chronic conditions outside of hospitals can save substantial amounts per patient. Additionally, POC diagnostics play a vital role in rural and underserved regions, improving access to essential healthcare.

Technological Innovation

Rapid innovation in biosensor technology, miniaturized devices, artificial intelligence, and cloud-connected platforms has transformed the POC diagnostic landscape. Devices today are more accurate, easier to use, and capable of transmitting data in real-time to healthcare providers.

Continuous glucose monitors (CGMs), portable PCR machines, lateral flow assays, and molecular diagnostic tools are examples of platforms revolutionizing the market. These tools offer high sensitivity and specificity while enabling integration with telemedicine and digital health ecosystems.

Segmentation Analysis

The global POC diagnostic market is segmented based on product type, sample used, mode of purchase, platform, and end user.

By Product:

The key product categories include blood glucose monitoring, infectious disease testing, cardiometabolic disease testing, pregnancy and fertility testing, hematology testing, and other niche areas. Among these, blood glucose monitoring is the leading category due to the widespread prevalence of diabetes.

By Sample Type:

Samples commonly used in point-of-care testing include blood, nasal or oropharyngeal swabs, urine, and others. Blood remains the most dominant sample type due to its versatility and reliability across different test types.

By Mode of Purchase:

The market is split between prescription-based and over-the-counter (OTC) products. While prescription diagnostics are used primarily in hospitals and clinics, OTC options such as glucose monitors and pregnancy tests support the growing home-care market.

By Platform:

Diagnostic platforms include lateral flow assays, dipsticks, microfluidics, molecular diagnostics such as PCR and isothermal nucleic acid amplification, and immunoassays. Lateral flow remains the most commonly used, but molecular diagnostics are growing rapidly due to their ability to detect complex pathogens accurately.

By End-User:

End users include hospitals, clinics, home care settings, assisted living facilities, and laboratories. With increasing demand for remote and outpatient care, the home care and clinic segments are expanding rapidly.

Country-Level Analysis

United States

The U.S. is the largest and most mature market for point-of-care diagnostics. The country’s high healthcare spending, strong innovation ecosystem, and widespread adoption of decentralized healthcare delivery make it a central hub for this industry. The presence of leading diagnostic companies, such as Abbott and Dexcom, has further contributed to rapid technological advancements and market penetration.

Moreover, the U.S. faces a significant burden of chronic diseases. For instance, millions of Americans are living with diabetes, heart disease, or neurodegenerative conditions like Alzheimer’s. This health burden is driving demand for both diagnostic and monitoring solutions that are accessible, accurate, and time-efficient.

Reimbursement policies, government funding, and a growing elderly population are also major contributors to the adoption of POC solutions.

Germany

Germany is among Europe’s strongest point-of-care markets. It benefits from a robust healthcare infrastructure, favorable reimbursement systems, and a regulatory framework that supports rapid approval and distribution of diagnostic tools. German consumers and healthcare providers are highly receptive to new technologies, particularly those that enhance early diagnosis and chronic disease management.

Germany’s long-standing leadership in healthcare R&D and its active role in developing precision diagnostics have positioned it as a European leader in this sector. The country’s emphasis on preventive care and efficiency further supports the adoption of point-of-care solutions in clinics, elderly care facilities, and at-home settings.

Commutator Analysis

The evolution of the POC diagnostic market is influenced by various shifting parameters that interact dynamically:

A transition in product types—from basic test strips to wearable and molecular diagnostics—has significantly increased the value per unit sold. This shift, along with the demand for multi-analyte platforms, is enhancing the overall revenue potential of the market.

A notable transformation is also occurring in sample types. While blood remains the primary medium, innovation in saliva and urine-based diagnostics is expanding accessibility and ease of use.

Additionally, platform preferences are changing. While lateral flow assays remain prevalent, more complex diagnostic platforms using microfluidics and PCR technologies are gaining traction due to higher sensitivity and expanded diagnostic capabilities.

Another crucial trend is the movement from prescription-only diagnostics to consumer-driven OTC models. This democratization of healthcare empowers patients and encourages early diagnosis, particularly for lifestyle-related conditions.

Lastly, the growth in home-based care and clinics as key end users is reshaping distribution strategies and business models across the industry. Companies are increasingly focusing on direct-to-consumer marketing and remote device support services to address this demand.

Press Release Conclusion

The global point-of-care diagnostic market is set to undergo a significant transformation over the next decade. With strong growth forecasted from USD 45.16 billion in 2024 to USD 73.08 billion by 2032, the sector is poised to play an integral role in redefining how healthcare systems approach diagnostics and disease monitoring.

As infectious diseases, chronic conditions, and aging populations continue to stress traditional healthcare systems, point-of-care solutions offer timely, cost-effective, and accessible alternatives. The adoption of innovative platforms, favorable policy environments in leading countries like the U.S. and Germany, and growing consumer preference for home-based care are all fueling the expansion of this market.

Healthcare stakeholders, including providers, manufacturers, investors, and policymakers, are encouraged to align strategies with this trend, invest in next-generation diagnostic technologies, and explore new service models that integrate point-of-care testing into mainstream care.

About Stellar Market Research:

Stellar Market Research is a multifaceted market research and consulting company with professionals from several industries. Some of the industries we cover include science and engineering, electronic components, industrial equipment, technology, and communication, cars, and automobiles, chemical products and substances, general merchandise, beverages, personal care, and automated systems. To mention a few, we provide market-verified industry estimations, technical trend analysis, crucial market research, strategic advice, competition analysis, production and demand analysis, and client impact studies.

Contact Stellar Market Research:

S.no.8, h.no. 4-8 Pl.7/4, Kothrud,

Pinnac Memories Fl. No. 3, Kothrud, Pune,

Pune, Maharashtra, 411029

+91 20 6630 3320, +91 9607365656

: Unveiling the Structural Mysteries of Biomolecules")

Leave a Comment